As we described in a previous article, the Global Cannabis Stock Index extended the bounce from November after the huge October loss, rallying 8.1% in December. That index was down 20.1% in 2023, which followed a record decline of 70.4% for 2022. In January, it rallied again, rising 12.2%, but it fell 6.0% in February to 8.55.

In this article, we summarize the performance of the other managed indices that New Cannabis Ventures offers to its readers. We discuss the performance of the American Cannabis Operator Index, Ancillary Cannabis Index and Canadian Cannabis LP Index. The one that was quite strong in August and in September but led the way lower in October and reversed in November, was the weakest in December and the strongest in January. Only one sub-sector managed a gain during February, and it was not the one that has been so strong.

American Cannabis Stocks Index

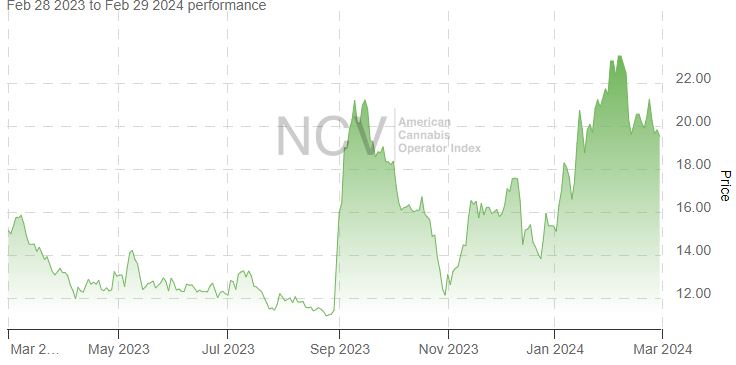

The American Cannabis Operator Index was quite strong in January after declining in December. In February, it plunged 9.2% to 19.51 :

In 2023, the index rallied 7.6% to 15.34 despite the overall weakness in cannabis stocks, and a late January close was the highest close in over a year. In 2024, this index is now up 27.2%:

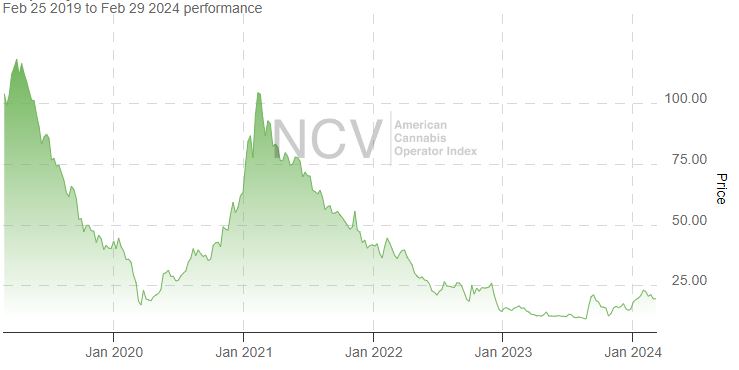

The index, which launched in October 2018, made an all-time low in August before soaring. It is still down a lot from when it launched:

The worst performing MSO in February was AYR Wellness (OTC: AYRWF) (CSE: AYR.A), which plunged 42.6%. Glass House Brands (OTC: CBSTF) (NEO: CBST) was the strongest stock, rising 12.1%.

In January, the index will have 14 members, with Schwazze (OTC: SHWZ) (NEO: SHWZ) joining.

Ancillary Cannabis Index

The Ancillary Cannabis Index was strong, gaining 2.3% to 12.99:

In Q4, the index lifted 0.9%. After a massive loss of 76.6% in 2022, it declined 10.9% in 2023 to 13.38, which was better than the Global Cannabis Stock Index. It is down 2.9% in 2024:

The index is down 87% since launching at the end of March in 2021:

The best performing stock in the index in February was Scotts Miracle-Gro (NYSE: SMG), gaining 16.8%. The worst stock was GrowGeneration (NYSE: SMG), declining 7.4%.

In January, the index will have seven members again. WM Technology (NASDAQ: MAPS) is replacing NewLake Capital Partners (OTC: NLCP)

Canadian Cannabis LP Index

The Canadian Cannabis LP Index fell again, dropping 10.0% to 54.35, a new all-time low:

The index, which fell 62.8% in 2022, was down 16.2% in 2023 to 60.85, and it is down 10.7% in 2024:

The LP index is down a lot from its peak:

The Canadian LPs trade mainly below C$1, with just just five of the stocks having a higher price at the end of February. 11 of the 19 stocks in the index closed below C$0.25. During February, Organigram (TSX: OGI) (NASDAQ: OGI) soared 24.1%, while Cronos Group (TSX: CRON) (NASDAQ: CRON) gained 4.4%. The other large LPs all fell. Canopy Growth (TSX: WEED) (NASDAQ: CGC) moved lower by 29.7%, while Aurora Cannabis (TSX: ACB) (NASDAQ: ACB) dropped 17.9%. Tilray Brands (TSX: TLRY) (NASDAQ: TLRY) experienced a 4.1% decline.

In March, the index will have 12 members, as 7 names that traded below $0.10 on 2/27 have been removed.

New Cannabis Ventures maintains four proprietary indices designed to help investors monitor the publicly-traded cannabis stocks, including the Global Cannabis Stock Index as well as the Canadian Cannabis LP Index. The third index, the American Cannabis Operator Index, was launched at the end of October 2018 and tracks the leading cultivators, processors and retailers of cannabis in the United States. Afterwards, we introduced the Ancillary Cannabis Index at the end of March 2021, reflecting the increasing number of publicly-traded companies providing goods or services to cannabis operators.

Be the first to comment